How do U.S. elections affect stock market performance?

Part 1 - S&P500

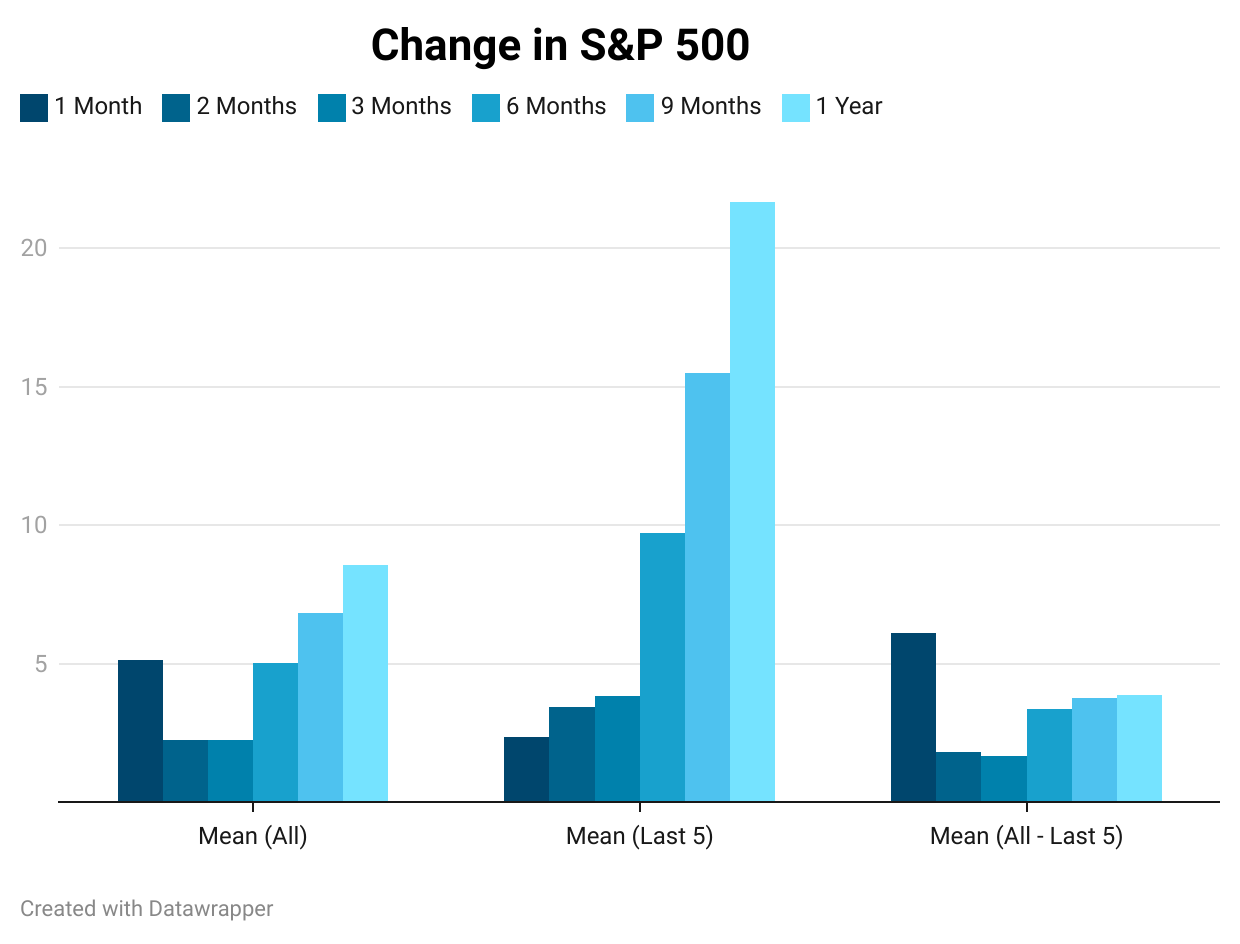

The market performance data used in this study go all the way back to 1945.

Please note that past performance is not a strong indicator of future stock market performance.

The market performance data used in this study go all the way back to 1945.

Please note that past performance is not a strong indicator of future stock market performance.